[

](https://substackcdn.com/image/fetch/$s_!AP1G!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ff2d892c3-49c7-489b-829c-20b7f5aa40be_1920x1080.png)

After six months and eight failed bids, the Ellisons made the Warner Bros. Discovery board an offer they couldn’t refuse. The potential Netflix acquisition would’ve been akin to fusing LVMH and Walmart — HBO’s prestige TV and Warner’s iconic IP, plus Netflix’s scale. Paramount Skydance buying WBD is the fusion of a dog and a car bumper traveling 80 miles an hour. Spoiler alert: It’s not going to end well.

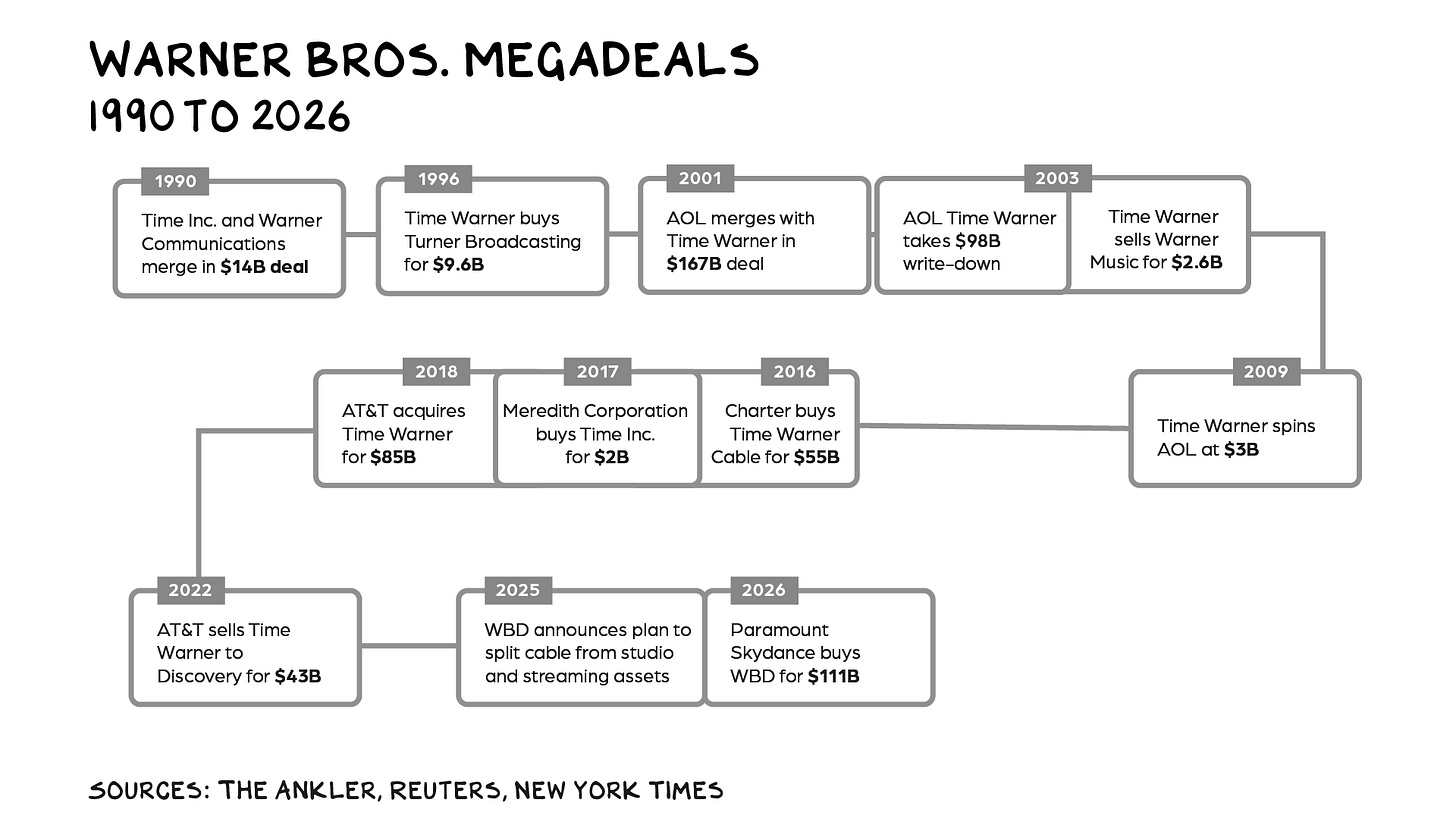

The story of Warner Bros. is a recurring masterclass in ego cosplaying corporate synergy. The company has undergone seven sales, mergers, or structural separations since 1967. The script remains the same: A new CEO decides Warner Bros. is the missing piece of their legacy, only to find they’ve partnered with a high-maintenance spouse who, after several years, leaves with half of everything the acquiring company used to own.

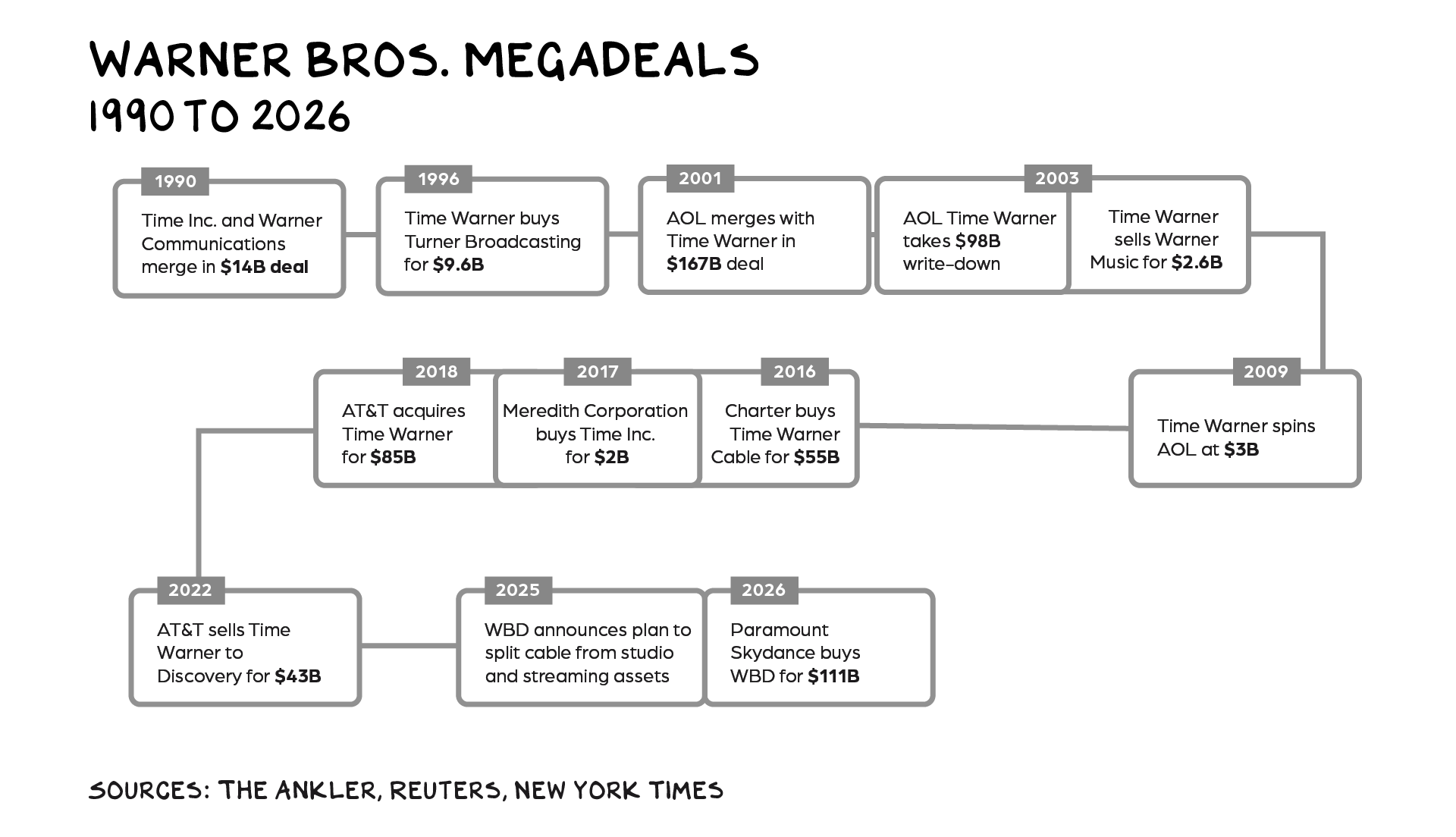

In 1989, Time Inc. and Warner Communications announced a “merger of equals” that would create Time Warner, the world’s largest media company to date. Things did not go as planned. First, Paramount’s hostile takeover attempt (past is prologue) scuttled the proposed stock swap and bid up the price. A year later, the deal closed at a $14 billion valuation — 13x EBITDA. To finance it, Time Warner took on $1.1 billion in annual interest payments to service $10.8 billion in debt. To avoid bankruptcy, Time Warner initiated “Project Glass,” a good bank / bad bank structure that put the company’s crown jewels (HBO, the film and television studios, and the cable assets) under a subsidiary, enabling it to receive cash infusions from outside investors. Meanwhile, the merger became a case study in clashing corporate cultures.

The Time Warner merger would provide a blueprint for future M&A disasters. Exhibit A: The ultimate destruction of shareholder value, AOL’s $167 billion merger with Time Warner. This time, the culture clash was between a legacy media company and an internet startup. The bigger issue, however, was that $167B valuation, premised on dot-com-era hallucinations. AOL’s market cap was nearly double Time Warner’s, while Time Warner had 5x the revenue. As the dot-com bubble began to deflate, news broke that AOL had been propping up its growth narrative by fraudulently inflating its advertising revenue. In the end, AOL Time Warner never came close to justifying a multiple of 25x to 30x EBITDA, and within a year of securing regulatory approval, the company took a historic $99 billion write-down. By 2003, Time Warner dropped AOL from its name, and in 2009 it spun off the unit. AOL’s value at the spin was $3B, a shadow of the $167B assigned just 10 years before.

But wait, there’s more.

In 2018 the synergy delusion struck again. This time, AT&T acquired Time Warner for $85 billion, creating WarnerMedia on the theory that its “dumb pipes” were the chocolate to Warner’s peanut butter, i.e., great content. But WarnerMedia struggled to make streaming profitable, its theatrical business was devastated by the pandemic, and once again there was a culture clash. The bigger challenge, however, was a 2.9x debt-to-EBITDA ratio, which trapped the telco in a pincer between dividend payments (a utility company’s raison d’être) and servicing the interest on $180 billion in debt. Ultimately, AT&T spun Warner, combining it with Discovery in a deal that netted the telco $43 billion — a 50% haircut.

The WBD sequel combined all the elements of the Worst Acquisition in History franchise. Another culture clash, this time between Discovery’s unscripted empire and Warner’s premium sensibilities, a wannabe mogul overpaying so he could cosplay as Robert Evans (ask Claude), and a 5x debt-to-EBITDA ratio. The good news? The sequel had a short runtime. CEO David Zaslav slashed costs, engineered a good bank / bad bank structure to spin WBD’s declining linear assets, and ultimately orchestrated a bidding war that restored shareholder value. As an operator, Zaz is Ed Wood (see: the worst branding decision in history, deprecating HBO), but as an investment banker, he’s Steven Spielberg.

[

](https://substackcdn.com/image/fetch/$s_!dYde!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ffb3cfc82-bcf1-4bf8-a2dc-04d75b31f4a9_1920x1104.png)

What do you get a nepo baby who already has Paramount? A: Warner Bros. According to one study that tracked 3,250 wealthy families over two decades, 90% lose their fortune by the third generation. Prediction: Larry Ellison’s great-grandchildren will never forgive him for providing a personal guarantee so David could go to the Oscars.

While the deal is priced at a multiple of 8x to 12x EBITDA, the “E” is anchored to a linear TV ecosystem that’s unraveling faster than regulators can approve the deal. WBD plus Paramount = 2x the linear headache. Wall Street is being asked to pay a premium for a story whose ending everyone already knows. And if valuation is the rock, leverage is the hard place. Last year the two companies generated a combined operating profit of $11 billion, before depreciation and amortization. The Paramount-WBD combo is two drowning men clinging to each other, hoping the combined weight of their $79 billion in debt will somehow act as a flotation device. It won’t, which is why Paramount’s debt was downgraded to junk status after the Ellisons “won” the WBD bidding war. With his new toy having a leverage ratio north of 6x, David Ellison has promised $6 billion in “synergies” within three years. (Netflix Co-CEO Ted Sarandos put the figure closer to $16 billion, after examining WBD’s books.) Synergies is Latin for layoffs. Additional “synergies” could be found by consolidating HBO Max with Paramount+ into a Franken-streamer no one asked for, merging CNN with CBS News, and going Cleopatra, i.e., selling one or both studio lots to real estate developers. (See: Fox selling 300 acres of its back lot to create Century City.)

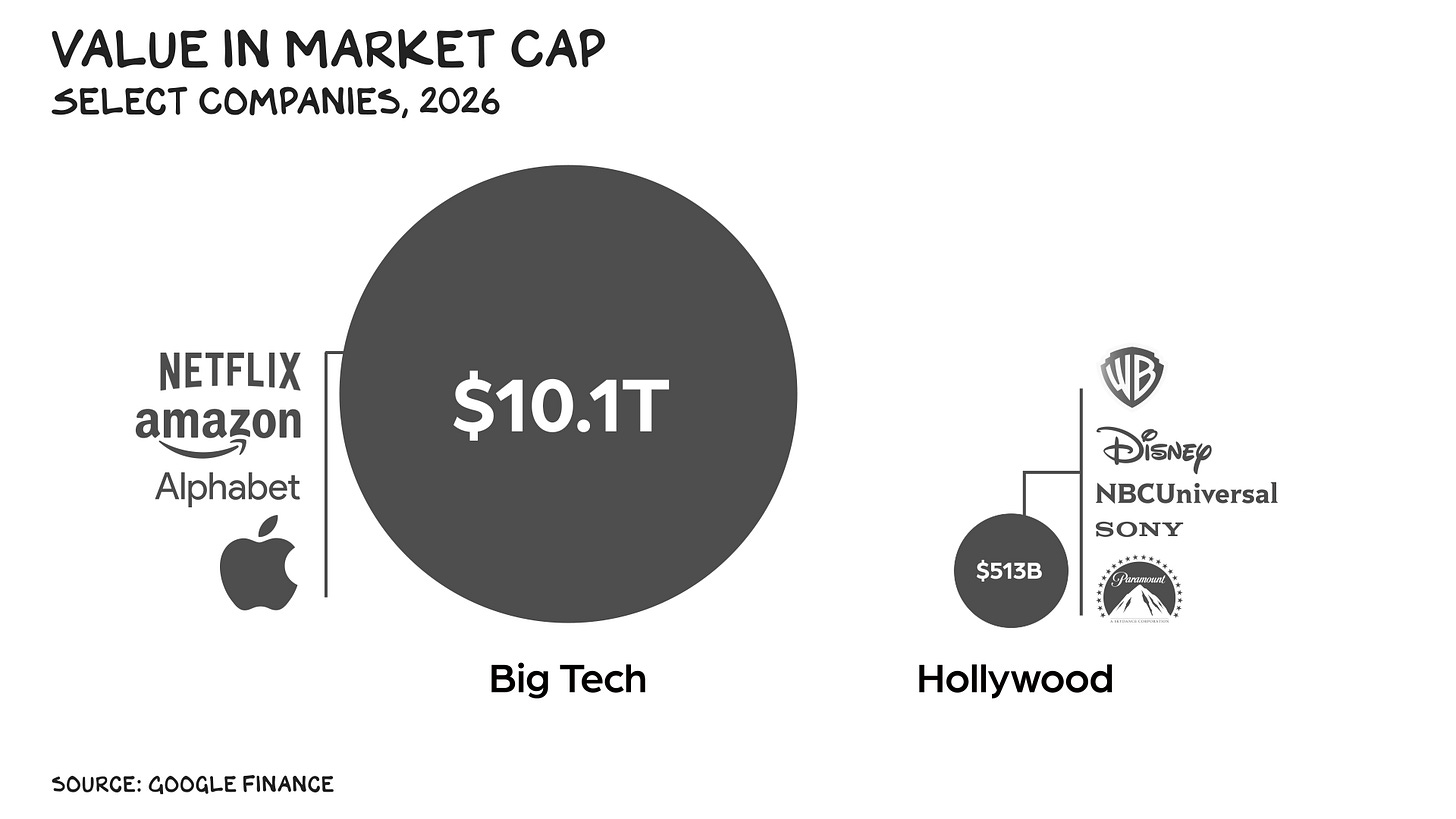

In Star Wars, when Grand Moff Tarkin tests the Death Star by destroying Alderaan, a pained Obi-Wan Kenobi says, “I felt a great disturbance in the Force, as if millions of voices suddenly cried out in terror and were suddenly silenced.” Big Tech is the Death Star, and Hollywood’s creative community is Alderaan. After acquiring Paramount, the Ellisons laid off 2,000 employees — 10% of the workforce. After acquiring WBD, David Ellison attempted to quell layoff fears among Warner employees, insisting the majority of cost-cutting would come from “non-labor sources.” Nobody believes that. It’s going to be difficult to cut billions in snacks.

While it’s not yet fully operational, but armed with a TikTok laser, the Ellisons are fixing their AI Death Star’s sights on Hollywood. For a sneak preview of coming attractions, see the credits of The Fantastic Four: First Steps. The Marvel movie employed 3,000-plus cast and crew members — more people than work at Lyft or Reddit. The Ellisons don’t care if Hollywood is ready for AI. They believe AI is ready for Hollywood. Paramount / WBD is ground zero. Amazon, Apple, Netflix, and YouTube won’t be collateral damage, they’ll be the beneficiaries. The Ellisons blow up Alderaan; Big Tech inherits the Empire.

[

](https://substackcdn.com/image/fetch/$s_!-ErO!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F70a3d934-5dc4-4883-ad71-b7d726407ad4_1920x1080.png)

After walking away from the WBD deal, Netflix’s stock popped 14%, partially reversing a 20% to 30% drop in the share price since the deal was first proposed. As a parting gift, Netflix pocketed a $2.8 billion break up fee, equivalent to 15% of its annual content budget. During the bidding war, Hollywood cast Netflix as the white knight and the Ellisons as the villains. Remarkable, given Hollywood’s 2023 work stoppage was called the “Netflix strike.” When I was pitching a television show, the money was better at Netflix, but everyone wanted to work for HBO, which punches above its weight in cultural relevance. The Ellisons won’t just burn HBO’s goodwill, they’ll napalm it with a cocktail of AI slop and arrogance garnished with fascist flourishes. In Hollywood, reputation is currency, and the Ellisons are broke.

But perhaps Netflix’s biggest win is that it may have thrown the competition into stasis. Despite using their relationship with President Trump as a cudgel, the Ellisons must still clear EU regulatory hurdles, as well as potential litigation from state attorneys general. They’ll likely get approval, as antitrust enforcers no longer break up behemoths, just delay their agenda. Nevertheless, history demonstrates that any deal to acquire Warner Bros. has a remarkably short shelf life.

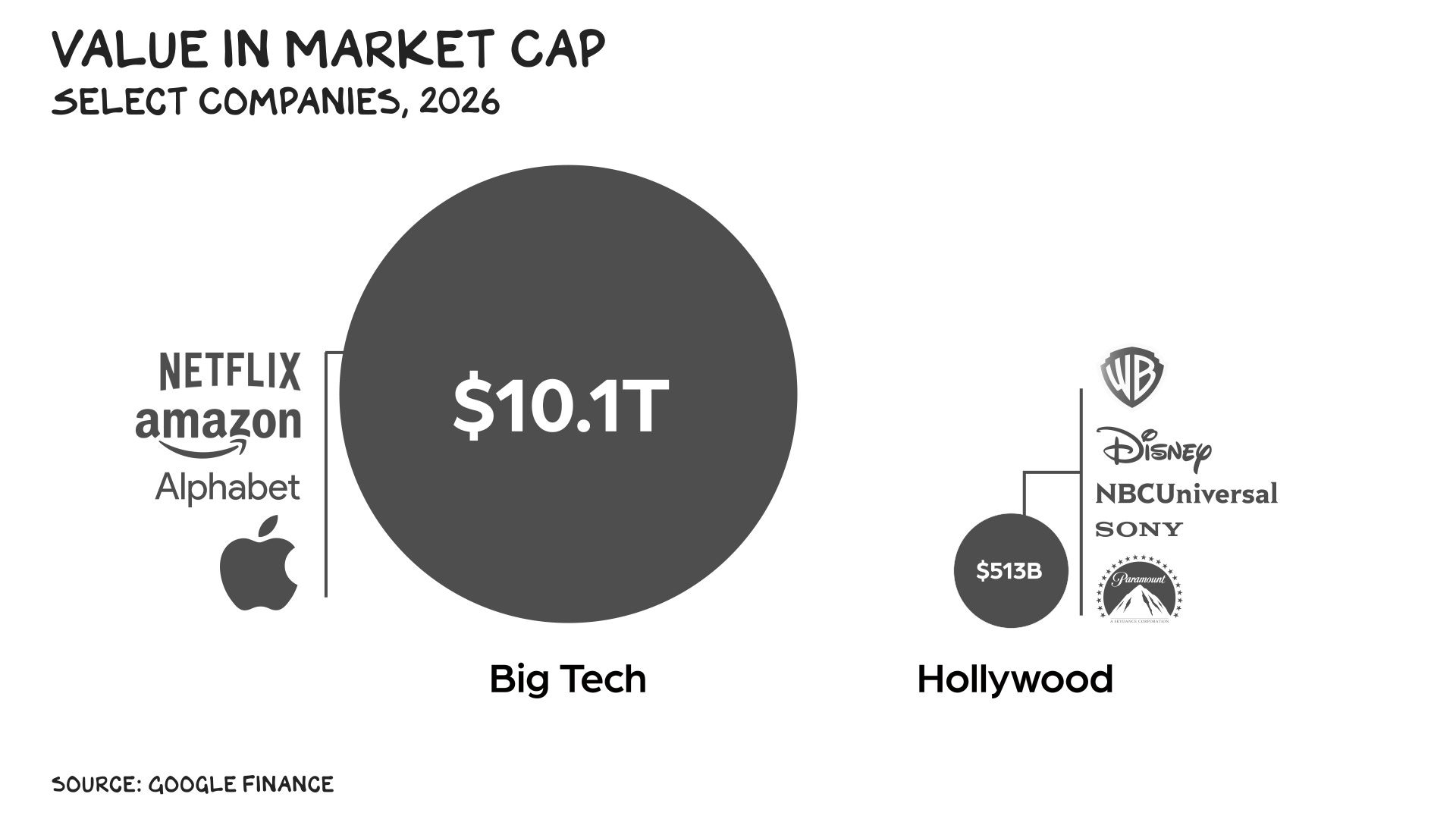

Ted Sarandos was on the verge of a transformative acquisition … and still is. But it’s not WBD. A decent test of value is to benchmark similar assets. By walking from the deal, Ted and Co. saved $121B, and their equity value has increased $60B since putting the WBD spliff down. Add the $3B break-up fee and you have an effective $184B (opportunity) cost for WBD. So, what could you get for $184B? A: The Mouse … Walt Disney Co. ($179B). A side-by-side comparison illuminates just how talented an auctioneer David Zaslav is, and suggests the Centerview bankers who talked Ellison into paying this price have a second career as psychedelic doulas. Let’s shine a light on the unexploded IED that is WBD.

For the same price, Wall Street would have you believe that WBD was the “value play.” It isn’t. It’s a value trap. Disney generated $21 billion in operating income last year on $91B in revenue — WBD registered $11B in operating income on $42B in revenue, and half of that came from a dying linear TV business that’s shedding subscribers. But the real gap isn’t in the financials — it’s in the moats. Disney has theme parks that print $8B in operating income annually with 60%+ incremental margins. WBD has ... CNN and TBS reruns. Disney owns the IP that dominates global culture: Marvel, Star Wars, Pixar, ESPN. WBD owns HBO (great) and a back catalog that hasn’t produced a billion-dollar franchise in a decade. Disney’s parks business alone — just the parks — is worth more than WBD’s entire enterprise value. You’re buying a recession-resistant, pricing-power machine with Disney. With WBD, you’re buying a melting ice cube of linear TV assets wrapped in $40B of debt trading at 5x leverage. One of these companies will be worth $300B in 10 years. The other will be sold for parts to Netflix. The second generation of wealth ensures that the third generation … isn’t. Shari Redstone, Edgar Bronfman Jr., and (now) David Ellison.

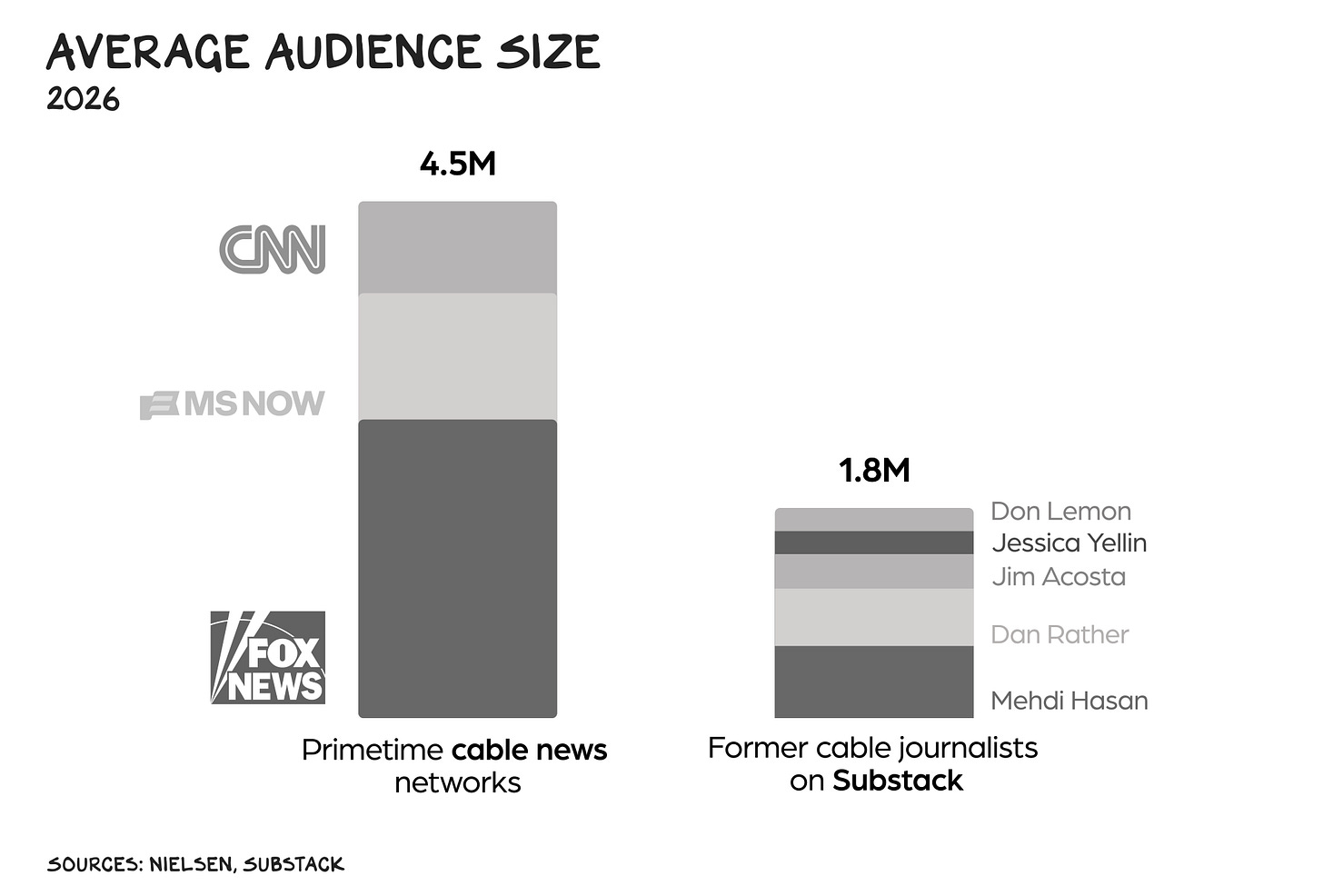

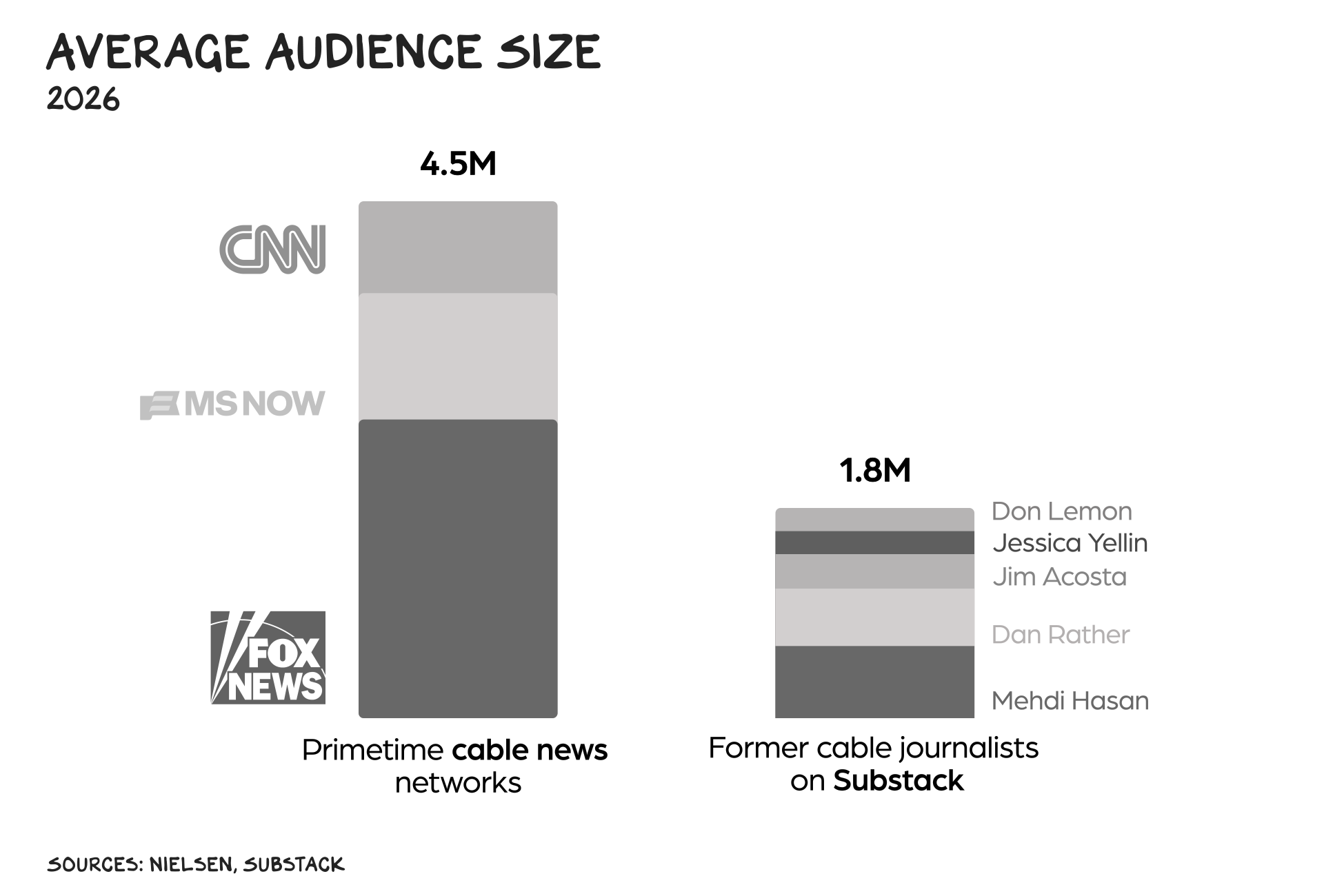

I’ve been having a lot of conversations with cable news anchors who are seeing their pay fall off a cliff. My advice is always the same: Seize the means of production, i.e., start a podcast, launch a Substack, etc. We’ve transitioned from a fossil-fuel-based economy to an attention economy, full stop. If you command attention, revenue follows. The Ellisons will do to CNN what they’re already doing to CBS News. At CNN, $3M/year anchors are a cost center on a bloated P&L. On YouTube or Substack, they’re platforms with 90% margins. The smart money isn’t betting on the logo on the building; it’s betting on the X-wing fighter, the individual talent with the firepower to knock out the Death Star before it can recharge and hit its next target. I know, I’m getting carried away with the Star Wars stuff. Whatever, my Bantha (i.e., newsletter).

[

](https://substackcdn.com/image/fetch/$s_!zqTJ!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F6ab89a15-d2c0-4a17-a5a1-2e0a561bc48d_1920x1300.png)

There are only two ways to make money in the media business: bundling and unbundling. We’re in a bundling phase. The question isn’t what the Ellisons will do with Paramount and WBD, but who will acquire those assets at fire-sale prices when their AI synergy narrative can no longer provide cloud cover for their pair of overleveraged legacy media companies. My prediction: We’ll see this movie again, starring Netflix, Apple, and Amazon as bargain hunters with delusions of grandeur that involve paying a failed CEO hundreds of millions for the right to fire hundreds of thousands of their employees. In Star Wars, the good guys blow up the Death Star. In Hollywood, you just wait for it to collapse under its own debt load. Same ending, lower production budget.

Life is so rich,

[

](https://substackcdn.com/image/fetch/$s_!0g2r!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F03baba44-8473-4c8d-a0eb-5c386d07cce8_1200x96.png)

P.S.

This Sunday, Kara Swisher and I will be in Minnesota for Resist and Unsubscribe. The event is sold out, but you can WATCH IT LIVE on Substack. Register here.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}